The journey toward financial security, especially in old age, remains a complex and uneven path for billions of people worldwide. Recent data offers a fascinating new perspective: Wealth and worry about financial security in old age do not always correlate. This blog explores the relationship between a country’s consumer class—the share of people spending $12+ per day—and the share of its population worried about financial security in old age.

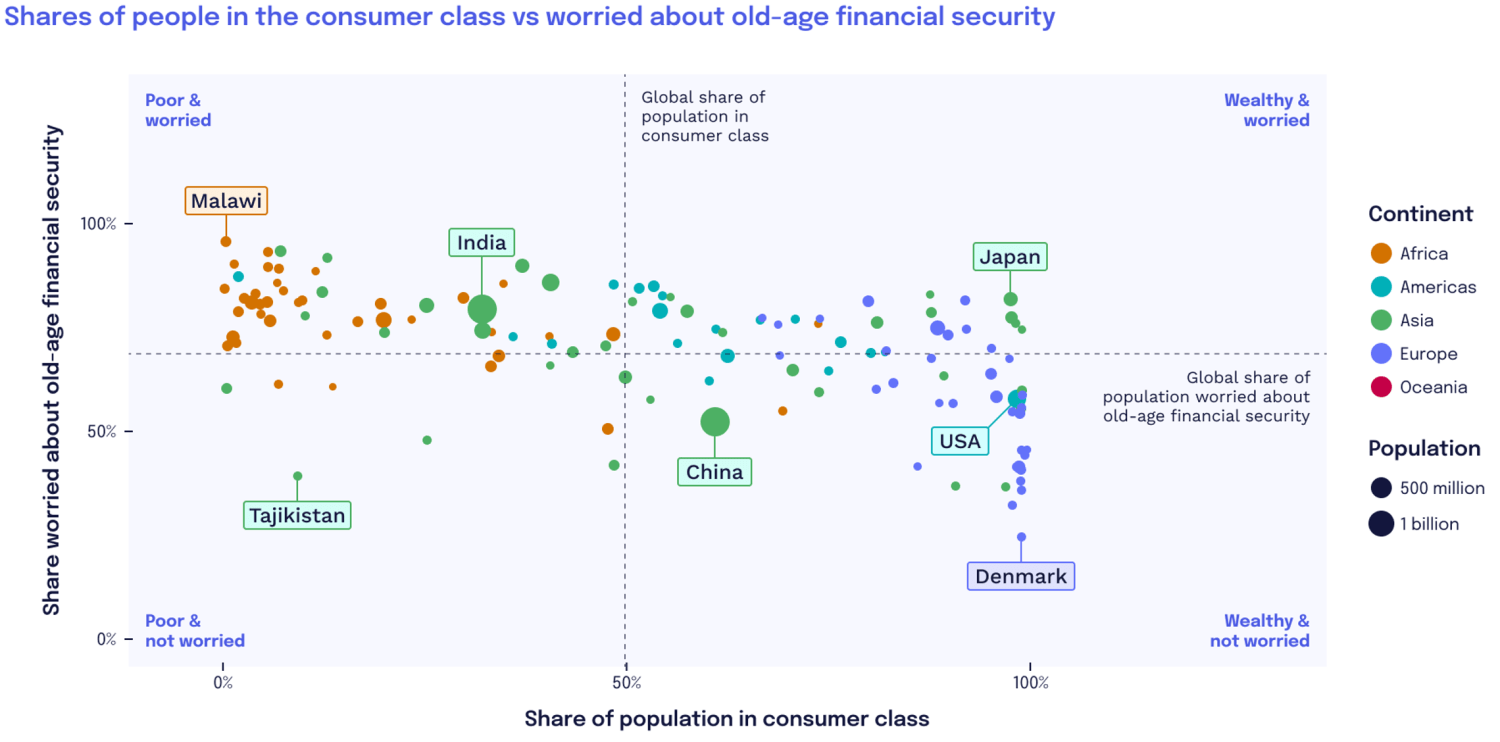

Figure 1 shows the relationship between the share of people in the consumer class and those worried about old-age financial security across countries. Each point represents a country, with the dotted lines marking global averages. Countries above the horizontal line have more people than average worrying about old-age finances, while those to the right of the vertical line have larger consumer classes. These patterns highlight the complex link between wealth and financial concerns.

Figure 1. Wealth does not always create peace of mind

Source: Author projections derived from World Data Pro and FINDEX data. Note: Consumer class figures are taken from the World Data Lab’s aggregation of household surveys in 184 countries. The World Bank’s FINDEX database tracks global financial inclusion and concerns.

The data tell us two stories

-

Wealth is important in alleviating worries about old-age finances.

In countries with higher shares of people in the consumer class, like Denmark, concerns about old-age financial security are minimal. Conversely, in Malawi, a country with almost no consumer class, almost everyone worries about finances in old age.

-

Old-age security is not only about income.

Wealth alone doesn’t guarantee peace of mind. Other factors—such as access to pensions, health care, inequality, and cultural attitudes toward saving—play a pivotal role in shaping financial confidence for older generations. For example, almost everyone in Denmark and Japan is in the consumer class, but Japanese households are particularly concerned about old-age finances. The United States has a far higher share of its population in the consumer class than China, yet a higher percentage of people in the U.S. are worried about their old-age finances. Tajikistan is an outlier, where the population does not seem to worry about its old-age financial situation despite the fact that households are relatively poor.

What to do

As Figure 1 shows, financial worry transcends income levels and geographic boundaries. Addressing this global challenge requires action on several fronts:

- Strengthening social safety nets: Both poor and wealthy countries can enhance financial security for vulnerable populations, like the elderly. Denmark stands out for its unique combination of financial prosperity and relatively low levels of worry, demonstrating how financial prosperity combined with a strong social safety net can alleviate financial anxieties.

- Promoting financial literacy: Even in wealthier nations, inadequate financial planning and understanding can fuel insecurity about old-age finances.

- Reducing barriers to financial inclusion: The success of innovations like mobile money in low-income countries demonstrates how technology can expand access to financial tools, which can help reduce worries about financial security.

The journey to financial security is not linear, but the global community can learn valuable lessons from contrasting experiences. By addressing the intertwined challenges of poverty and financial worry, we can work toward a future where financial security in old age is not a privilege but a shared reality for everyone.

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Are the wealthy less worried about old age?

February 7, 2025