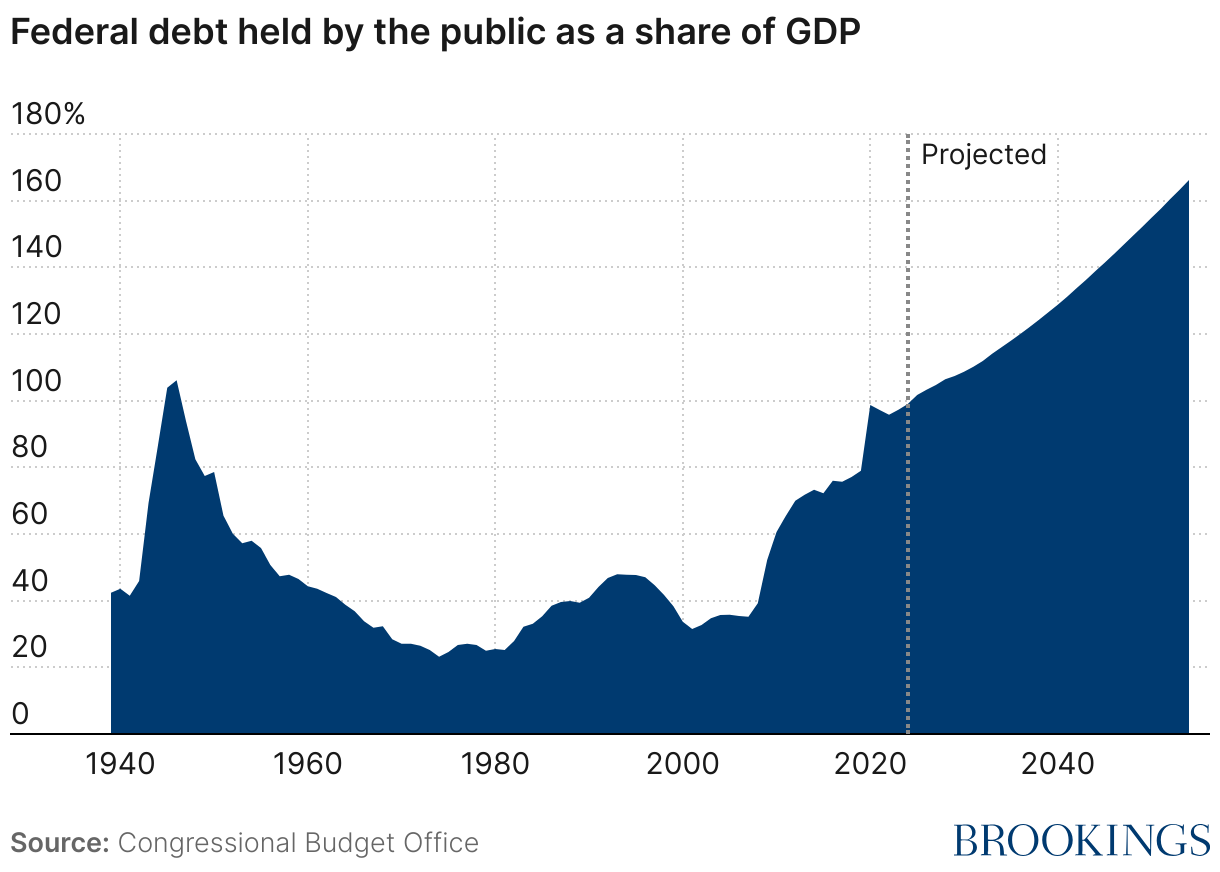

The federal debt, measured against the size of the U.S. economy, is at levels not seen since World War II. Without changes in tax and spending laws, it is projected to climb steadily and indefinitely. The current tax code won’t generate nearly enough revenue to cover the rising projected costs, namely those related to retirement and health benefits promised to an aging population. So far, however, the U.S. government has been able to borrow trillions of dollars a year at interest rates that are moderate by historical standards. Analysts warn, however, that our nation’s growing debt will inevitably lead to a crisis.

In a new paper, “Assessing the Risks and Costs of the Rising U.S. Federal Debt,” we address the costs of debt and the likelihood of such a fiscal crisis in coming decades. The analysis will be discussed at a Brookings event on February 12, 2025.

Here is a Q&A that summarizes the main points of the paper.

Q. Starting with the basic economics, what are the consequences of federal debt persistently growing faster than the overall economy?

A. Even if the U.S. avoids a crisis, future generations will be worse off than they would be if we slowed the growth of federal debt. We are borrowing today largely to finance current consumption, benefiting current generations. This borrowing will push up interest rates and crowd out increasing amounts of private investment. Less investment means slower productivity growth, which in turn means the living standards of future generations will be lower than they would otherwise be. Thus, rising debt as a share of GDP over the coming decades means that future generations will be worse off than if less debt was accumulated, although economic growth means that future generations will probably still be better off than current ones.

Q. There is a lot of talk on Wall Street, in Congress, and in the press about the risk of a “fiscal crisis.” How do you define that term?

A. We define a fiscal crisis as a sudden, large, and sustained downturn in demand for Treasury securities relative to supply that triggers a sharp and persistent spike in interest rates, probably accompanied by a steep fall in the value of the U.S. dollar and equity markets. We do not mean a temporary spike in Treasury yields that dissipates quickly, which could happen if, for example, fiscal or monetary policymakers respond to a spike in rates by taking effective action to bring down interest rates. While the higher cost of borrowing from a fiscal crisis would inflict substantial pain on the economy over time, the more worrisome risk is that a breakdown in Treasury markets could cause a global financial crisis that erodes asset values, destabilizes financial institutions, and pushes economies into recession. Furthermore, the U.S. response might be sharp increases in taxes and cuts in government spending that could add to the economic costs from the financial market breakdown.

Q. What could spark a fiscal crisis?

A. There is no specific level of debt that will abruptly lead markets to fear that the U.S. will default on its debt or otherwise significantly impair its value. Instead, we see several sources of risk, each described below. We view each of these scenarios as unlikely, but it would be foolhardy to suggest that they could not occur. In each case, the depth of the resulting crisis would depend critically on the response of policymakers. We acknowledge the considerable uncertainty about how Congress, the Federal Reserve, and the administration would respond to a sharp shift in demand for Treasury debt relative to supply in the future.

Q: What does it mean for the U.S. to “default on its debt or otherwise significantly impair its value?”

A. In essence, default means not making timely interest or principal payments. That said, there are various degrees of non-payment. At one end of the range would be a delayed payment on a small subset of bonds due to a temporary debt limit impasse. At the other end would be a default on the entire outstanding stock of debt, perhaps done strategically because doing so was expected to improve the fiscal and economic outlook. In addition, a sharp and unexpected increase in inflation would lower the real cost of the debt, but—like default—it would make future borrowing much more expensive.

Q. What if a big holder of U.S. Treasuries—say China—abruptly sells its holdings?

A. China owns about $1 trillion of U.S. federal debt, about 3% of the total outstanding. That’s about half the amount the Federal Reserve has shed from its balance sheet in its current round of Quantitative Tightening (QT—the unwinding of the bond-buying Quantitative Easing of the pandemic), which Fed economists suggest will not have large effects on U.S. borrowing rates or threaten financial stability. The QT analysis suggests that a $1 trillion sell-off by China wouldn’t have large effects, provided, of course, that such a move didn’t trigger widespread selling of U.S. Treasuries by others. If the sell-off was limited but still caused temporary disruptions in financial markets, the Fed has the capacity to purchase unlimited quantities of Treasuries to stabilize the market. Importantly, however, the Fed would have to assure investors that it wasn’t abdicating its mandate to maintain low and stable inflation; presumably, it would eventually unwind its purchases and allow interest rates to rise in response to the reduction in demand for U.S. Treasuries.

Q. Could political gridlock or brinksmanship lead investors to fear the U.S. Treasury will miss payments on its bonds?

A. If Congress failed to raise the debt ceiling and that limited Treasury’s ability to pay its bills (as has come close to happening in recent years), Treasury would be forced to decide which bills to pay. Most analysts anticipate that the Treasury would make interest and principal payments on U.S. Treasury debt a priority, but it’s not clear it has that legal authority, and no one can be sure what any particular administration would do. The effects of a binding debt limit on financial markets largely depend on how long the episode lasts, how any legal challenges are resolved, and how investors regard the likelihood of a repeat once the debt ceiling is raised. Other threats to default would likely play out in a similar way. If investors believed default was a legitimate possibility, interest rates would likely spike. Whether that episode turned into a protracted fiscal and financial crisis would depend on whether and how quickly policymakers changed course.

Q. What about a perception that the Fed is abandoning its mandate to maintain low and stable inflation as a strategy to reduce the real value of the debt and thus limit the need to raise taxes or cut spending?

A. If investors became worried that the President or Congress was successfully pressuring the Fed to abandon its mandate to keep inflation under control, the response in interest rates could be significant and a crisis could be triggered. But the reality is that inflation doesn’t do much to address the nation’s fiscal challenges. The ability of inflation to lower the debt-to-GDP trajectory depends on the maturity of the debt—short-term debt would be rolled over at ever-higher interest rates. More significantly, the primary issue for the U.S. over the next three decades is not paying interest on the stock of debt per se, but large, projected gaps between non-interest spending and revenues (primary deficits). Even if inflation could somehow eliminate all the accumulated debt (which it can’t), most of the fiscal challenges would remain.

Q. Could Congress cut taxes and raise spending so much that investors think that strategic default is a near-term risk?

A. None of the scenarios projected for the U.S. come remotely near the debt levels and trajectories where default is likely to be a smart strategy. A default on all outstanding U.S. Treasuries would almost surely precipitate a global financial crisis. Further, because about 70% of the debt is held by Americans, most of the savings from foregone interest payments would be at the expense of U.S. investors. In addition, the U.S. would likely lose access to capital markets for some time. That would mean that spending would immediately have to fall to the level of revenues and that the U.S. would not be able to borrow during downturns or in response to other economic shocks. Finally, defaulting on our debt would mean relinquishing the U.S.’s status as a global financial leader, with far-reaching consequences that extend well beyond economics.

However, there may be a level of debt so high where the benefit of defaulting on our debt would outweigh those costs. If Congress cut taxes and raised spending so much that strategic default actually appeared to be plausible, the results could be quite dire. In addition to a likely financial crisis, interest rates on U.S. Treasuries would spike, making it very costly to roll over federal debt and making default more likely.

It is worth considering the role of the Fed in this situation. The Fed can help restore confidence in Treasuries in the case of a run that is not based on fundamentals—when most sellers are offloading Treasuries primarily out of fear that others will do the same. If some investors begin to worry about the trajectory of fiscal policy and interest rates start to spike, the Fed can likely stabilize Treasury markets temporarily. By doing so, it can provide fiscal policymakers with a window to reassure markets that a default is not on the table—perhaps by taking meaningful steps to address the nation’s long-term fiscal challenges.

However, if the fiscal situation were to deteriorate to the point where a strategic default becomes a plausible strategy, the Fed’s ability to intervene effectively would be severely constrained. As part of the federal government, the Fed would struggle to maintain credibility if investors believed there was a significant probability of default. If conditions deteriorate to the extent that investors are unwilling to lend to the Treasury even at very short maturities, they would likely view holding deposits at U.S. banks—backed by reserves at the Fed—as equally unacceptable.

Q. What is your bottom line? Is the United States at risk of a fiscal and financial crisis because of the debt?

A. Ultimately, the nation must address its fiscal challenges by raising taxes, cutting spending, or doing both. Delaying action benefits current generations at the expense of future ones, but, in our view, likely will not lead to a crisis. A fiscal crisis could be triggered if politicians take irresponsible actions like threatening to default, threatening to undermine essential institutions (such as the Federal Reserve), or threatening to balloon the deficit in ways that suggest no commitment to future generations.

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

What are the risks of a rising federal debt?

February 12, 2025